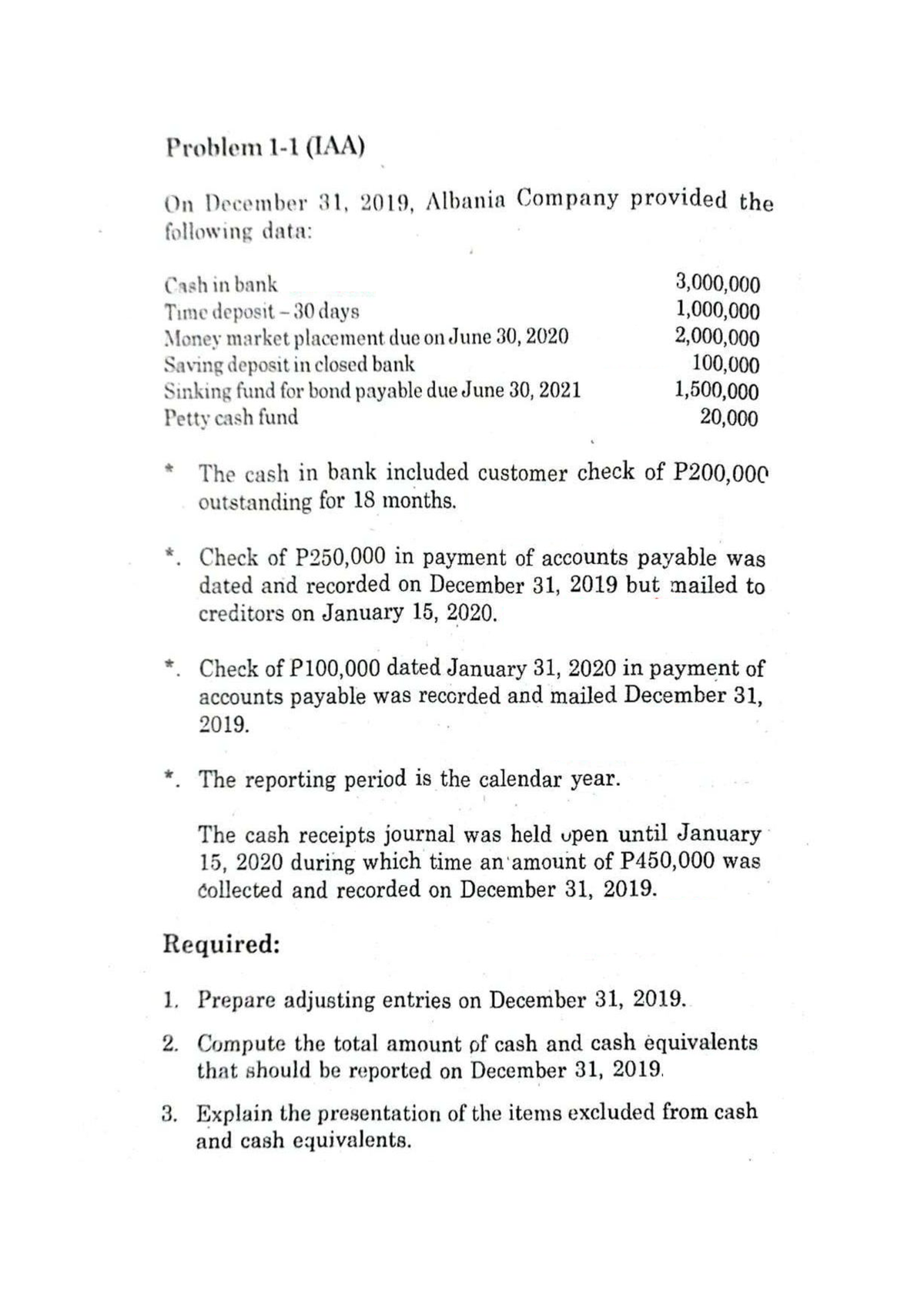

Particularly, when your home is worth $3 hundred,000 along with home financing harmony away from $150,000, your property guarantee try $150,000.

Next, determine how far family security you could potentially realistically obtain out of and how much cash in debt you truly need to combine. This involves totaling their a great expense towards credit cards, signature loans, automobile financing, and other high-desire capital to ascertain the quantity you owe.

Loan providers generally fool around with a personal debt-to-earnings ratio out-of 43% to determine how much you can afford so you’re able to obtain. As an instance, in case the month-to-month earnings is actually $ten,000 while already spend $step 1,500 a month with the most of your home mortgage, you could probably be able to obtain definition liquidate security up to an extra $2,800 monthly.

Lastly, determine what sorts of house security funding is the best for your immediately following meticulously shopping certainly one of different lenders and you can financing products and researching the eye cost, costs, and you may cost terms.

Domestic security options for debt consolidation reduction

Like magic, right here is the lowdown on three popular domestic equity money car you can realize for debt consolidation motives.

House collateral financing to own debt consolidation reduction

In the event that approved, you might tap into the fresh guarantee your house has accumulated. House guarantee funds is second mortgages that really work similarly to number one mortgages.

You are billed a predetermined otherwise varying interest, your commit to a set repayment name (generally speaking anywhere between five and 30 years), therefore make month-to-month dominating and you can focus costs per month immediately following you personal towards the loan. Of many mortgage lenders, banking institutions, borrowing unions, and other creditors bring house collateral finance.

HELOC to have debt consolidation reduction

A great HELOC was a great rotating personal line of credit you should buy for those who have collected at least level of collateral on the household (always you would like about 20% collateral built up getting eligible for an effective HELOC). That have a great HELOC, you have got a blow period, aren’t spanning the newest type of credit’s very first ten years. More than this stage, you could potentially extract currency (household equity) from the personal line of credit should you wanted a long time as you never go beyond the set borrowing limit.

Within the draw months, you are just needed to make lowest costs on one due focus towards finance you elect to borrow. Acquire no cash and you may owe little (unless of course their lender assesses an inactivity fee). Immediately following the mark stage concludes, you aren’t allowed to obtain even more cash unless of course your own bank authorizes a good HELOC renewal.

The next phase is new cost stage, tend to lasting 10 so you can two decades, more and this go out you ought to pay-off your own owed equilibrium.

Cash-out refinance to have debt consolidation reduction

With a finances-aside re-finance, your replace your most recent no. 1 home mortgage Sumter installment loan no credi checks no bank account with a brand new large real estate loan. You take cash out at the closure according to the difference in cash between those two money (deducting one settlement costs).

You can prefer a predetermined interest rate otherwise an adjustable-speed financial (ARM). But the majority of people do not pull the fresh new lead to to the a profit-away refi unless of course the pace is lower than its most recent financial loan’s rate of interest.

Which is the best choice?

Very first, determine how much obligations we wish to combine additionally the attract rates on the latest financing. This should help you see whether a house security loan, HELOC, otherwise bucks-out refi offers a much better rate of interest and you will words getting your specific condition, Silvermann advises.

Next, think about your monthly income and determine simply how much your have enough money for spend monthly. This will help you decide between a house equity financing otherwise cash-away refinance with a fixed commission plan or good HELOC with a variable commission schedule.

Add Comment

Only active ALBATROSS Racing Club members can post comments